In the Loop – July 10, 2026

“In The Loop” is designed to give you a short update reflecting major developments, earnings, and investment trends across some core Equity Income and Growth holdings. All clients should be aware that individual buy/sell recommendations will be conveyed directly to you on an individual basis. Have a great weekend.

My short-term predictions rarely work so here are a few historical facts:

History continues to provide a constructive backdrop for the second half of the year. Since World War II, the S&P 500 has advanced in the second half 77% of the time after posting a positive first half, with that success rate increasing to 81% when first-half gains exceeded 5%. This year also stands out historically, as the S&P 500 recorded 24 new all-time highs through June 25, placing 2026 among the 20 strongest first halves since World War II. In those comparable years, the index generated an average 6% gain during the second half and finished higher 80% of the time. While these statistics are encouraging, investors should still expect periods of volatility. Midterm election years have historically produced larger swings, with 45% of second halves experiencing pullbacks of 5% or more, reminding us that strong long-term trends often include meaningful short-term corrections.

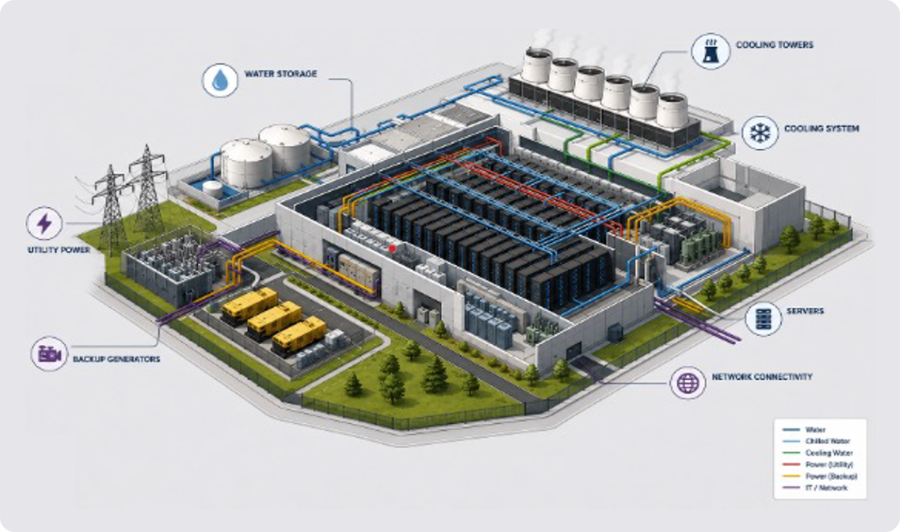

One of the most important developments in today’s market is that artificial intelligence is no longer just a software story, it has become a full-scale industrial investment cycle. Just a few years ago, hyperscale cloud providers collectively spent roughly $162 billion on capital expenditures. Today, annual spending is on pace to approach $600-$750 billion in 2026, with many industry forecasts suggesting investment could move even higher over the next several years. This is no longer simply a technology cycle; it is a generational buildout of physical infrastructure requiring enormous investments in semiconductors, networking, power generation, electrical equipment, cooling systems, construction, and data centers. In our view, investors should increasingly think of AI as an infrastructure theme rather than a software theme.

The drivers behind this spending continue to strengthen. AI adoption is expanding across both consumers and enterprises, while reasoning models and autonomous AI agents require significantly more computing power than earlier generations of large language models. At the same time, token usage continues to accelerate at an extraordinary pace as AI becomes integrated into everyday workflows. Each new generation of models demands more inference-time compute, creating a virtuous cycle where higher usage leads to greater infrastructure investment, which in turn enables even more powerful AI capabilities.

This week’s earnings from the memory industry reinforced that trend. Micron Technology delivered another strong quarter, highlighting continued demand for high-bandwidth memory (HBM) and AI-related DRAM despite investors taking profits following the stock’s significant run over the past year. Samsung Electronics also reported results that reflected ongoing strength in AI memory demand, although investors remained focused on execution and competitive positioning within HBM rather than near-term earnings alone. The market’s reaction illustrates that expectations have become exceptionally high, but importantly, neither company suggested that AI infrastructure demand is slowing. Instead, both reinforced the view that memory remains one of the primary bottlenecks supporting the AI investment cycle.

Another notable development came from SK Hynix, which completed the largest-ever foreign ADR listing in U.S. history, raising approximately $26.5 billion. The decision to access U.S. capital markets reflects both the enormous capital requirements of the AI memory industry and management’s desire to broaden its shareholder base while benefiting from the premium valuations often afforded to leading U.S.-listed semiconductor companies. The offering also gives U.S. investors direct exposure to one of the world’s leaders in high-bandwidth memory, an area that remains supply constrained as hyperscalers continue expanding AI infrastructure.

For investors, the most important question is no longer simply which AI model will win, but rather where every dollar of AI capital spending ultimately flows. Every new AI data center requires advanced chips, HBM memory, advanced packaging, servers, networking equipment, power distribution, cooling systems, and reliable electricity before a single AI query is ever processed. Those physical bottlenecks remain where we believe the most durable long-term investment opportunities exist.

This continues to reinforce our U.S. Resiliency investment framework. Rather than concentrating solely on AI software companies, we remain focused on the mission-critical businesses enabling this unprecedented infrastructure buildout—companies involved in electricity generation, grid modernization, networking, advanced semiconductors, industrial construction, and critical physical infrastructure. As AI transitions from a technology theme into an industrial economy theme, we believe owning the companies that build the backbone of this ecosystem offers a compelling way to participate in what may become one of the largest capital investment cycles in modern history.

Individual Company Updates

Talen Energy remains one of the most direct ways to invest in the growing power needs of AI data centers. The company continues to benefit from increasing demand for reliable baseload electricity and its strategic generation portfolio, with investors focused on additional opportunities to serve hyperscale customers. We continue to view TLN as a unique infrastructure asset positioned at the intersection of AI and power.

GE Vernova continues to execute well as one of the premier beneficiaries of the global power infrastructure buildout. Demand for gas turbines, grid equipment, and electrification solutions remains strong as utilities and hyperscalers invest heavily to support AI-related electricity demand. Investors will closely watch second-quarter results later this month for updates on backlog, margins, and future orders.

Vertiv remains one of the highest-quality infrastructure providers supporting AI data centers through advanced cooling, power management, and thermal solutions. The company recently expanded its manufacturing footprint and completed the acquisition of ThermoKey, further strengthening its ability to meet accelerating customer demand. We continue to view Vertiv as a critical “picks and shovels” provider for AI infrastructure.

nVent continues to benefit from sustained investment in electrical infrastructure, grid modernization, and data center expansion. Its portfolio of electrical connection, enclosure, and thermal management products remains well positioned as AI facilities require increasingly complex power distribution systems. We believe nVent remains an underappreciated beneficiary of the long-duration electrification cycle.

Eaton continues to see robust demand across electrical equipment, power distribution, and intelligent power management as utilities, industrial customers, and hyperscalers expand capacity. The company’s strong backlog and broad exposure to AI infrastructure, commercial construction, and grid modernization reinforce our view that Eaton remains one of the highest-quality industrial compounders in the market.

Fabrinet continues to benefit from increasing demand for high-speed optical networking components used throughout AI infrastructure. As hyperscalers upgrade networks to support larger AI clusters, Fabrinet remains an important manufacturing partner for leading optical equipment suppliers. We believe the company remains well positioned to benefit from continued upgrades to 800G and next-generation 1.6T networking technologies.

Formidable Asset Management (“Massey Romans Capital”) is an investment adviser registered under the Investment Advisers Act of 1940. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, the Firm cannot guarantee the accuracy of the information received from third parties.

The opinions expressed herein are those of the Firm and may not actually come to pass.Author

Paul MasseyRelated posts

In the Loop – June 5, 2026

Markets pulled back sharply on Friday as stronger-than-expected economic data pu

In the Loop – July 3, 2026

Tomorrow, America celebrates its 250th birthday. As I was thinking about what to