In the Loop – June 5, 2026

“In The Loop” is designed to give you a short update reflecting major developments, earnings, and investment trends across some core Equity Income and Growth holdings. All clients should be aware that individual buy/sell recommendations will be conveyed directly to you on an individual basis. Have a great weekend.

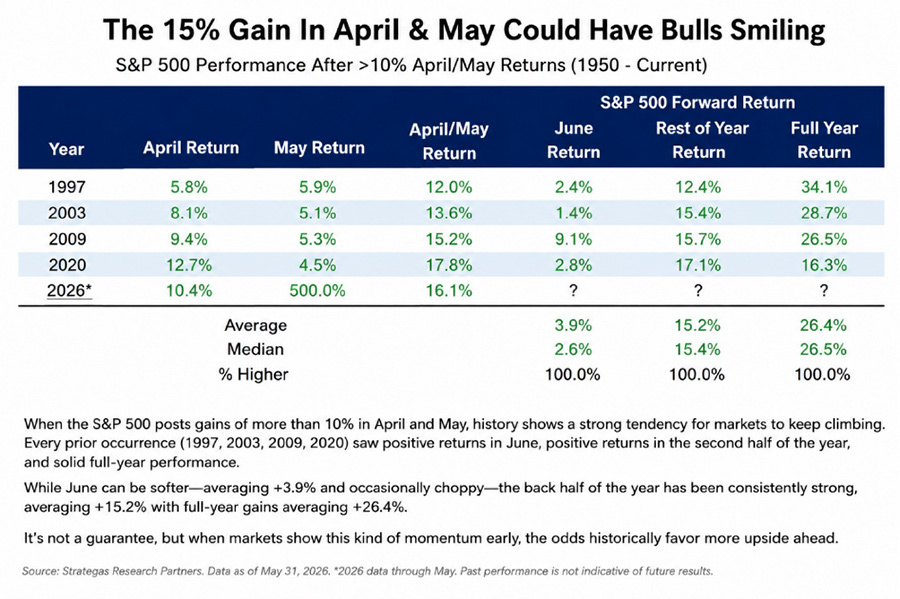

Markets pulled back sharply on Friday as stronger-than-expected economic data pushed Treasury yields higher and reduced expectations for near-term Federal Reserve rate cuts. The reaction was felt most acutely in technology and semiconductor stocks, which have led the market higher throughout the AI-driven rally. Broadcom’s earnings and outlook also contributed to profit-taking across the semiconductor complex, providing a catalyst for investors to lock in gains after an extraordinary advance.

From a technical standpoint, the pullback is not unexpected. Many semiconductor and AI infrastructure stocks have posted gains of 50% to 100% in a matter of weeks, leaving sentiment stretched and positioning crowded. Historically, periods of rapid appreciation are often followed by corrections of 5% to 10%, even during powerful bull markets. Importantly, market breadth held up far better than the headline indexes suggested, indicating that selling was concentrated in a handful of large technology names rather than representing broad-based liquidation across the market.

Investors often ask whether a sharp Friday decline marks a market bottom. History suggests there is no consistent pattern. While some corrections end on Fridays, many require several additional trading sessions for institutional investors to complete repositioning and for buyers to re-emerge. The more important signals will be whether Treasury yields stabilize, whether semiconductor leaders such as NVIDIA, Broadcom, AMD, and Micron begin to find support, and whether broader market participation remains healthy.

Our base case is that this represents a consolidation within an ongoing bull market rather than the beginning of a major downturn. The fundamental drivers behind the AI infrastructure buildout remain intact, corporate earnings continue to grow, and capital spending plans from hyperscalers remain near record levels. In fact, some of the strongest bull markets in history have experienced multiple sharp pullbacks along the way. While additional volatility over the next several days would not be surprising, we view this move as a healthy reset after one of the most powerful technology rallies since the late 1990s rather than a change in the long-term investment outlook.

Markets rarely move in a straight line. After an exceptional run in AI and semiconductor stocks, a period of consolidation is both normal and constructive. We remain focused on the long-term themes driving our portfolios and view volatility as a feature of investing, not a flaw.

One of the week’s most important developments was Alphabet’s announcement of an $80 billion capital raise to accelerate its AI infrastructure buildout. Rather than signaling weaker demand, the move reinforces a key theme we have discussed for months: demand for AI computing capacity is growing faster than available supply. The industry’s biggest challenge today is not finding customers—it is building enough power generation, data centers, networking equipment, advanced semiconductors, and packaging capacity to meet demand. This continues to support our focus on companies occupying critical bottlenecks throughout the AI ecosystem.

The market is also beginning to shift from the “AI excitement” phase to the “AI execution” phase. Investors are increasingly focused on which companies can successfully deliver the infrastructure required to support the next wave of AI adoption. In many ways, today’s environment resembles past industrial buildouts where the greatest opportunities emerged among the companies providing the essential tools, equipment, and infrastructure needed to enable growth.

Looking ahead, investors are preparing for what could become one of the largest and most anticipated public offerings in market history as SpaceX moves closer to an IPO. Beyond the excitement surrounding the company itself, a successful offering would signal strong investor appetite for innovation, technology, and long-term growth opportunities. It could also help reopen the IPO market for a new generation of private technology leaders.

This week’s volatility appears more consistent with normal profit-taking than a change in the broader market narrative. Economic conditions remain reasonably constructive, corporate investment in AI continues to accelerate, and infrastructure constraints across power, networking, semiconductors, and data centers remain significant. We continue to believe the most attractive opportunities are found among the businesses enabling this transformation rather than simply participating in it.

Individual Company Updates

NVIDIA used Computex 2026 to reinforce its vision of becoming the full-stack leader in AI infrastructure. The company introduced RTX Spark, a new AI-focused PC platform that combines an Arm-based CPU with its Blackwell GPU, marking NVIDIA’s first major push into the personal computer processor market. While the PC opportunity is likely a longer-term growth driver, the more important development was the continued production ramp of the next-generation Vera Rubin AI platform and the launch of Vera, NVIDIA’s first internally developed CPU designed specifically for AI workloads.

Together, NVIDIA’s expanding portfolio of GPUs, CPUs, networking, software, and AI tools strengthens its position at the center of the AI ecosystem. The company is also extending its reach into robotics, autonomous systems, and AI agents, creating additional long-term growth opportunities. The key takeaway is that NVIDIA continues to deepen its control of the AI infrastructure stack, positioning itself to benefit from rising demand for increasingly complex AI applications.

Formidable Asset Management (“Massey Romans Capital”) is an investment adviser registered under the Investment Advisers Act of 1940. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, the Firm cannot guarantee the accuracy of the information received from third parties.

The opinions expressed herein are those of the Firm and may not actually come to pass.Author

Paul MasseyRelated posts

In the Loop – February 6, 2026

This past week lived up to its “House of Pain” label, with the sharpest loss

In the Loop – March 20, 2026

Before I get into the weeds, I want to remind all long-term investors that since

In the Loop – February 27, 2026

The calm at the index level hides strong currents beneath the surface. The S&P 5