In the Loop – April 17, 2026

“In The Loop” is designed to give you a short update reflecting major developments, earnings, and investment trends across some core Equity Income and Growth holdings. All clients should be aware that individual buy/sell recommendations will be conveyed directly to you on an individual basis. Have a great weekend.

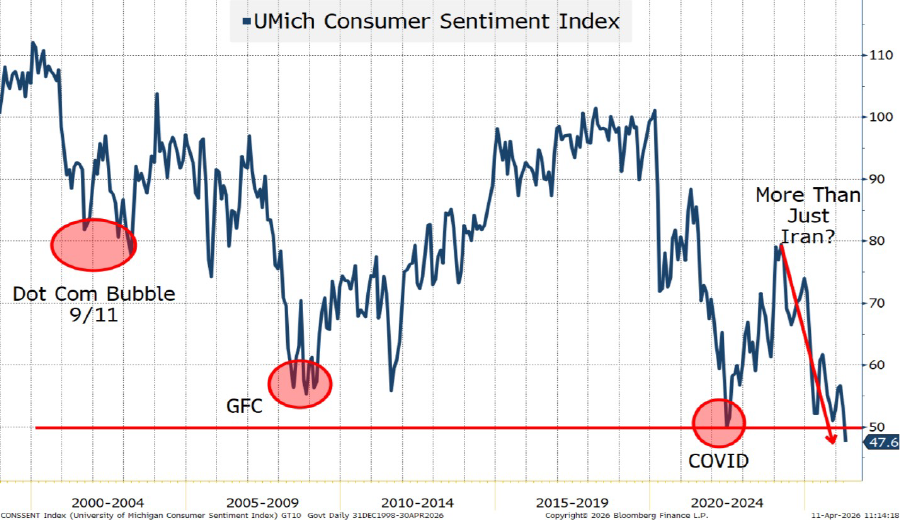

Two weeks ago, we included a picture of the Fear & Greed Index showing Extreme Fear in the Markets. We closed the explanation of the chart with a Warren Buffet quote “Be Greedy when others are Fearful”. Since then, The S&P 500 and Nasdaq Composite both closed at new all-time highs, with the Nasdaq extending its winning streak to 12 straight sessions. Strength was evident across semiconductors, energy, chemicals, industrials, managed care, food, and Chinese technology names. This week I want to share a picture of The University of Michigan Consumer Sentiment Survey. This survey began in 1946. According to Bloomberg, it is now reading 47.6. When sentiment is at today’s levels, you’re operating in a regime only seen a handful of times in ~80 years.

At first glance, it seems contradictory that the stock market is pushing toward all-time highs while consumer sentiment sits near recessionary lows—but the disconnect reflects two very different realities. Markets are being driven by global corporations, institutional capital, and a powerful investment cycle led by AI, infrastructure, and energy, while consumer sentiment reflects the day-to-day experience of households dealing with higher borrowing costs, persistent inflation, and housing affordability pressures. In other words, the market is forward-looking and tied to earnings and capital spending, whereas consumers are reacting to current conditions and rising costs of living. This divergence has created a “two-speed economy,” where large-cap, capital-intensive sectors are thriving even as the average consumer feels strained. Historically, these gaps tend to resolve through either improving sentiment or slowing markets, but in the near term they often lead to increased dispersion and rotation beneath the surface. For investors, the key takeaway is that today’s market strength is being fueled more by investment than consumption. This is a meaningful shift that favors companies tied to infrastructure, energy, and long-term capital spending trends.

This can also explain why credit card companies, homebuilders and restaurants have lagged. Our Pre-War/ US Resiliency framework has helped us avoid these sectors.

Interest rates moved modestly higher this week, with Treasury yields edging up across the curve as investors balanced a resilient economic backdrop against ongoing uncertainty around the path of future Federal Reserve policy. Meanwhile, initial jobless claims came in below expectations, reinforcing the view that the labor market remains firm and suggesting the broader economy continues to show underlying strength despite pockets of mixed data.

President Trump announced that Israel and Lebanon have reached a 10-day ceasefire following their first direct diplomatic talks in decades, held in Washington. As of this morning, Iran says the Strait of Hormuz is open to commercial shipping, but vessels must follow a route set by Iranian authorities. The U.S. says its blockade of Iranian ports remains in place, so the situation is still tense.

Individual Company Updates

JPMorgan delivered a strong quarter, supported by robust trading and investment banking activity amid elevated market volatility, which more than offset modest pressure in net interest income. Loan growth has remained stable and credit quality continues to normalize without signs of meaningful deterioration, reinforcing confidence in the bank’s underwriting discipline. Management maintained a constructive outlook, highlighting resilient consumer and corporate balance sheets while acknowledging macro uncertainty tied to rates and geopolitics. Importantly, JPM’s scale, diversified revenue streams, and capital strength continue to position it as a primary beneficiary of market dislocation and client activity, reinforcing its role as a core holding in periods of elevated volatility.

Bank of New York Mellon reported a solid quarter, with results driven by strength in fee-based businesses, particularly asset servicing and custody, as market levels and client activity improved. Net interest income came in ahead of expectations, supported by stable deposit trends and disciplined balance sheet management. The company continues to benefit from its position at the center of global capital flows, with higher rates and market volatility acting as tailwinds for both fees and client engagement. Management remains focused on expense control and operating leverage, while ongoing strategic investments in platforms and technology aim to enhance long-term growth. Overall, BK’s capital-light model and sensitivity to market activity position it well in the current environment.

ASML reported a strong quarter, beating expectations on both revenue and earnings, driven by continued strength in demand for advanced semiconductor equipment tied to artificial intelligence and data center expansion. Revenue reflected solid year-over-year growth and margins above guidance. Management raised its full-year outlook, now expecting 2026 revenue of €36–40 billion, as chipmakers accelerate capacity investments to meet surging AI demand. The company highlighted that demand continues to outpace supply, reinforcing ASML’s position as the critical “picks-and-shovels” provider to the global semiconductor ecosystem, with customers such as TSMC, Samsung, and Intel expanding orders. ASML’s monopoly in EUV lithography and its central role in enabling next-generation chips continue to underpin a durable growth trajectory tied directly to the AI infrastructure buildout.

Formidable Asset Management (“Massey Romans Capital”) is an investment adviser registered under the Investment Advisers Act of 1940. The information presented in the material is general in nature and is not designed to address your investment objectives, financial situation or particular needs. Prior to making any investment decision, you should assess, or seek advice from a professional regarding whether any particular transaction is relevant or appropriate to your individual circumstances. Although taken from reliable sources, the Firm cannot guarantee the accuracy of the information received from third parties.

The opinions expressed herein are those of the Firm and may not actually come to pass.Author

Paul MasseyRelated posts

In the Loop – June 20, 2025

Even though it was a shorten trading week with the markets closed for Juneteenth

In the Loop – July 18, 2025

With The S&P500, Dow Jones Industrial Average and the Nasdaq 100 bumping up on A

In the Loop – February 27, 2026

The calm at the index level hides strong currents beneath the surface. The S&P 5